The Directorate General of Taxes rewrites its taxpayer-supervision playbook

Circular SE-8/PJ/2026 replaces four separate circulars and becomes the operating manual for how the DGT will monitor compliance under PMK 111/2025.

Issued 15 July 2026 · Signed by Bimo Wijayanto, Director General of Taxes · Effective on the date of stipulation · Implements PMK 111/2025

| In brief

▪ SE-8/PJ/2026 is the DGT’s internal operating manual for taxpayer supervision. It took effect on 15 July 2026 and repeals SE-14/PJ/2019, SE-11/PJ/2020, SE-05/PJ/2022 and SE-9/PJ/2023. ▪ Supervision runs on three tracks: registered taxpayers, unregistered taxpayers, and territorial data collection across each office’s economic area. ▪ Material compliance review is now sorted into three named types with fixed clocks: automatic (1 working day), simple (10 working days), and comprehensive (22 working days, extendable to 44). ▪ The taxpayer’s SP2DK response window remains 14 days, extendable by 7. The DGT must close the file (LHP2DK) within 44 working days of delivering the SP2DK, extendable by 22. ▪ The whole process runs inside Coretax (the DGT Supervision Administration System). |

What the circular does

SE-8/PJ/2026 is implementing guidance (juklak) for PMK 111/2025. That Ministerial Regulation, in force since 1 January 2026, gave taxpayer supervision and the SP2DK a Minister-level legal basis for the first time; before it, the rules on how the DGT watches compliance lived only in internal circulars. The circular tells the DGT’s own officers how to plan supervision, carry it out, follow it up, quality-assure it, and evaluate it across every level of the organisation.

The circular does not, by itself, create new obligations for taxpayers. What it changes is how the DGT will use the powers PMK 111/2025 granted, and that changes what a taxpayer should expect when a letter arrives. Bimo Wijayanto signed it on 15 July 2026, and it repeals the four circulars that previously governed extensification, field data collection, compliance supervision, and concrete-data follow-up.

EXHIBIT 1

Supervision now runs on three parallel tracks

| Track | Who it targets | How the DGT acts |

| Registered-taxpayer supervision | Taxpayers already holding an NPWP, split into strategic and other | Requests for explanation of data (P2DK via an SP2DK), advisory letters (imbauan), and reprimands (teguran) |

| Unregistered-taxpayer supervision | Persons and entities that meet the subjective and objective tests but have not registered | P2DK in the course of extensification, leading to registration or a notice of examination result (SPHPP) |

| Territorial supervision | Economic activity within each tax office’s working area | Data collection (KPD) in four modes: area-based, analysis-based, function-incidental, and non-function |

SOURCE: SE-8/PJ/2026, General provisions and §C; PMK 111/2025 Art. 3.

The framework the DGT will operate

Governance sits with Compliance Committees (Komite Kepatuhan) at three levels: head office, regional office (Kanwil), and tax office (KPP). These committees set the annual priority lists that drive everything downstream: the supervision priority list (DPP), the extensification priority list (DPE), and the data-collection priority list (DPKPD). A taxpayer lands on one of these lists through a risk assessment run on the DGT’s Compliance Risk Management engine, not at an individual officer’s whim.

Review happens in two layers. Formal compliance review looks at whether filing, payment, and registration were done on time and in full. Material compliance review asks the harder question: whether the tax reported was actually correct. The DGT then splits material review by timing. Current-year obligations fall under Pengawasan Pembayaran Masa (PPM); obligations for years already closed fall under Pengawasan Kepatuhan Material (PKM). Which bucket a matter sits in decides which review type applies and how many years are on the table.

Taxpayers are formally classed as strategic or other. Strategic taxpayers are every taxpayer registered at the Large Taxpayer, Special Jakarta, and Medium Tax Offices, plus the largest contributors at Pratama offices designated by the regional head. Strategic status matters in practice because those taxpayers receive comprehensive review by default.

The circular also names the surveillance methods the DGT may use, and the list is broader than the old regime spelled out: remote-sensing valuation, web scraping, geotagging, media and journal mining, mirroring of audit and investigation results, information networks built through village-level police liaisons (Bhabinkamtibmas), and “taxation partnership” arrangements.

From four circulars to one

The clearest change is consolidation. Four circulars that used to sit apart, each with its own vocabulary, now live in a single document.

EXHIBIT 2

SE-8/PJ/2026 repeals and absorbs four separate circulars

| Repealed circular | What it governed | Now handled in SE-8/2026 as |

| SE-14/PJ/2019 | Extensification procedure | Unregistered-taxpayer supervision |

| SE-11/PJ/2020 | Field data collection and data-quality assurance | Territorial supervision through KPD |

| SE-05/PJ/2022 | Taxpayer compliance supervision | Registered-taxpayer supervision and material review |

| SE-9/PJ/2023 | Follow-up on concrete data | Automatic review and the concrete-data workflow |

SOURCE: SE-8/PJ/2026 §F (closing provisions).

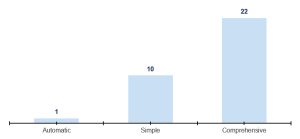

Three material-review tracks, each on its own clock

The old circular referred to research and to P2DK, but it did not carve material review into defined types with statutory deadlines. SE-8/2026 does exactly that, and the deadlines are short.

- Comprehensive review is the full look at every tax for a prior year. It works through the taxpayer’s risk profile, the reporting and payment record, the business process behind tax-invoice input and output, the financial statements, and the arm’s length of any related-party pricing. The base clock is 22 working days from the supervision order; it runs to 44 when a related-party pricing test is part of the review.

- Simple review is narrower: arithmetic and comparative checks, equalisation analysis, and application-of-law checks over some or all taxes. The clock is 10 working days.

- Automatic review is a tightly limited check against concrete data, and it must close in 1 working day.

Comprehensive review is not reserved for the largest taxpayers alone. It is triggered for every strategic taxpayer, and for any other taxpayer who meets a risk criterion. The trigger list is worth reading as a self-assessment: high risk; related-party transactions; membership of a group; reorganisation or business restructuring; a loss reported on the annual income-tax return; high-wealth individuals; recipients of a preliminary refund; turnover above Rp4.8 billion; recipients of a tax facility; or the KPP head’s own judgement.

EXHIBIT 3

Material review runs on fixed statutory deadlines

Working days from the supervision order to the review report (LHPt), before any extension

The 22-day clock extends to 44 working days when the review includes an arm’s-length (transfer-pricing) analysis.

SOURCE: SE-8/PJ/2026 §E.4, material compliance review within PKM.

What changed from the 2019–2023 regime

Six shifts matter for anyone advising taxpayers.

- One document, one vocabulary. Extensification, field data collection, compliance supervision, and concrete-data follow-up now share a single set of definitions and one workflow.

- A named taxonomy with hard clocks. Material review is now automatic, simple, or comprehensive, each with a fixed deadline of 1, 10, or 22 working days. The old regime left the timing loose.

- An explicit PPM / PKM split. Current-year monitoring and prior-year material review are now separated, and the split governs which review type applies and over how many years.

- Coretax as the system of record. Supervision runs through the DGT Supervision Administration System (the Coretax supervision module), and the circular only falls back to the legacy system where that module is not yet live.

- Formalised quality assurance. Two checkpoints now bracket the work: current QA (CSQA) while a case is open, and post QA (PSQA) after it closes, each run by dedicated teams at head office, Kanwil, and KPP.

- A firmer legal footing. Because the parent PMK 111/2025 lifted supervision and the SP2DK to a Ministerial basis from 1 January 2026, the instruments the DGT uses now rest on regulation rather than on an internal circular alone.

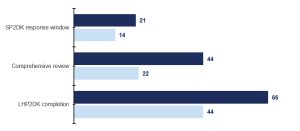

The compliance clock a taxpayer actually faces

For a taxpayer, the operative part of the circular is the SP2DK sequence. The letter is delivered through the taxpayer’s Coretax account; if the DGT delivers it another way, it must do so within 3 working days of issuing it. From a defined start date, the taxpayer has 14 days to respond, and may extend that by 7 more days by filing a written notice before the first window closes.

A taxpayer can respond more than once inside the window, and each response is minuted in a record of proceedings (BAP2DK). Silence carries a cost. If no response comes, the DGT can move to a visit (Kunjungan), then a discussion (Pembahasan), and finally a closing report (LHP2DK) that recommends audit or a preliminary-evidence examination. The DGT must issue that LHP2DK within 44 working days of delivering the SP2DK, extendable by a further 22. If, by then, the taxpayer has neither filed nor corrected the return in line with the BAP2DK, the file moves to audit or bukti permulaan.

EXHIBIT 4

The statutory clocks, base and maximum with extension

Base window and the maximum with extension, in days

▪ Base window ▪ Maximum with extension

The SP2DK response window is measured in calendar days; the comprehensive-review and LHP2DK windows are measured in working days.

SOURCE: SE-8/PJ/2026 §E.4, issuance of the SP2DK, receipt of the response, and the LHP2DK.

Why the DGT’s questions will be sharper

The circular ties territorial data collection to six data-quality dimensions, and only data that passes validation flows forward into supervision. The practical message for taxpayers is that the DGT is cross-checking asset, income, cost, debt, and equity data against the return before it ever writes to anyone. One of the tests, uniqueness, literally checks whether a bank deposit, a mortgage, or business income already appears on the taxpayer’s SPT.

EXHIBIT 5

Six quality tests every data point must pass before it drives a case

| Dimension | What it checks | Example from the circular |

| Completeness | All required data fields are recorded | Land or building data carries a plot ID or certificate number and a photo of the asset |

| Validity | Data matches the required format, type, and range | A vehicle record carries a plate number in the correct format and a value at fair or acquisition cost |

| Timeliness | Data carries a period and is not time-barred | Collection in 2025 on a 2023 sale, where assessment is not yet time-barred |

| Uniqueness | No duplicated records | A deposit, a mortgage, or business income is confirmed not already reported on the SPT |

| Consistency | Names, addresses, and linked items follow the standard | Bank interest expense implies a matching bank loan that must also be on record |

| Accuracy | The subject’s identity and figures are correct | Acquisition, sales, turnover, and taxable-object values reconcile to NPWP, NIK, name, and address |

SOURCE: SE-8/PJ/2026 §E.6, data-quality dimensions for KPD validation.

What taxpayers should do now

- Treat every SP2DK as a 14-day clock, not an open letter. Diarise the deadline and the 7-day extension the moment the letter lands in Coretax.

- Answer on substance, in writing, and get it minuted. A weak or missing response is precisely what escalates a file to audit or preliminary-evidence examination.

- Self-assess against the comprehensive-review triggers. Turnover above Rp4.8 billion, related-party dealings, group membership, a restructuring, a reported loss, a preliminary refund, or a tax facility each puts the full review in play; keep the file ready.

- Keep transfer-pricing and business-characterisation files contemporaneous. Comprehensive review explicitly includes transfer-pricing analysis, so documentation prepared after the fact is worth far less.

- Reconcile Coretax data before the DGT does. Assume third-party asset and income data has already been matched to the return through the six quality tests.

- Watch territorial exposure. Unregistered activity, informal premises, and un-geotagged assets are squarely in scope, and the DGT can register a taxpayer or confirm PKP status ex officio.

- Mind the concrete-data clock. Where a case sits close to the five-year assessment expiry, the DGT compresses its timelines and may proceed straight to audit without any P2DK.

EXHIBIT 6

A readiness checklist for the new supervision regime

| Action | Trigger to watch |

| Calendar the SP2DK deadline and extension | An SP2DK appears in the Coretax account |

| Prepare a substantive, minuted written response | Any data or explanation request from the KPP |

| Assemble the comprehensive-review file | Turnover > Rp4.8B, related parties, group, loss, refund, or facility |

| Refresh transfer-pricing documentation | Related-party transactions in any open year |

| Reconcile return data against Coretax records | Before year-end and before responding to any letter |

| Register premises and confirm PKP status | New or informal place of business in scope |

SOURCE: Mul & Co analysis of SE-8/PJ/2026.

How Mul & Co can help

The firm advises on SP2DK response drafting and deadline management, comprehensive-review readiness including transfer-pricing files and business characterisation, Coretax data reconciliation, and representation in discussions and visits. For a review of your exposure under SE-8/PJ/2026, contact your engagement partner at Mul & Co.

This update summarises SE-8/PJ/2026 for general information and is not legal or tax advice. Article and section references are to the circular as issued on 15 July 2026. Apply the rules to specific facts with professional advice.

For further information and taxation queries, please reach to :

Email : info@mul-co.com

WA : +62 82249384918